XVA · CVA / DVA / FVA / MVA / KVA / LVA

Counterparty risk

done right.

Multi-factor Monte Carlo, priced on the CSA discount curve. At CSA level we simulate a full VM and IM collateral grid across all paths, deriving accurate EPE, ENE, and exposure profiles. Funding costs, credit spreads, and CSA specificities — thresholds, MTA, cheapest-to-deliver — flow directly into each XVA component. On-premises or in the Cloud.

| Id | CVA | DVA | FVA |

|---|---|---|---|

| Portfolio | 426,358 | -211,508 | 84,210 |

| P: ENTITY2 | 12,708 | -6,140 | 2,180 |

| CP: BANK2 | 2,124 | -978 | 340 |

| CP: BANK13 | 824 | -322 | 108 |

| CP: BANK6 | 242 | -108 | 31 |

| CP: BANK14 | 33 | -12 | 4 |

Full Coverage

From model to metric — complete pipeline

Every step from calibration to aggregation runs on distributed infrastructure. No black boxes — drill down to deal and leg level on any metric.

Monte Carlo Pipeline

Hybrid Monte Carlo engine with correlated diffusion across all risk factors — IR, FX, credit spreads, equity. Native pricing models or plug in your own library. Calibrated per CSA for accurate collateral discounting.

Expected Positive Exposure — CP: BANK13

Collateral Management

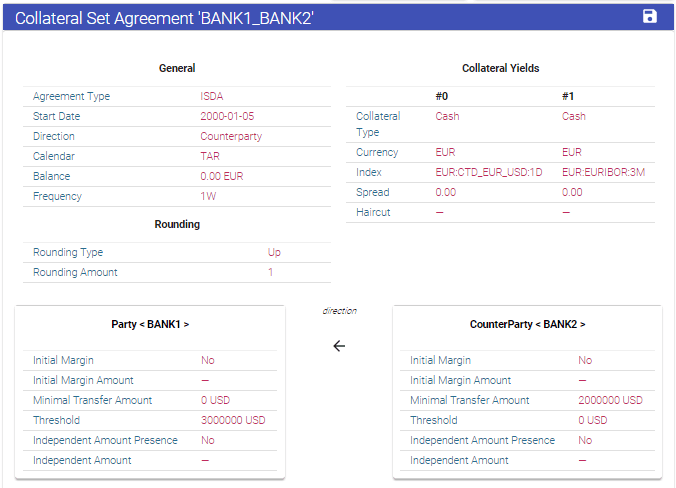

Full CSA simulation at path level — VM and IM collateral grids computed across all Monte Carlo scenarios. CSA specificities drive accurate exposure and funding cost attribution.

- MTA, MPOR, rounding

- VM & IM simulation

- Multiple CSA discounts

- Cheapest-to-deliver

- Collateral asymmetry

- Break clauses

Around XVA

Sensitivities & Hedging

Compute XVA delta, gamma, and vega across all risk factors. Use to construct hedging portfolios that offset your XVA exposure.

- IR, FX, CO & credit spread sensitivities

- Integrate with your front-office hedging flow

Reallocation to Deals

Each deal's marginal contribution to portfolio CVA, DVA, and FVA is computed and visible at deal and leg level — enabling accurate front-office charge attribution and pricing of new trades.

- Drill down to deal and leg level

- Marginal XVA for pre-trade pricing

- Allocation across netting sets

XVA Insights

Automatic attribution.

Every day, every move.

When your CVA moves overnight, Everix decomposes the change into factors — so you know exactly how much came from new trades, market moves, collateral adjustments, or configuration changes.

Advanced Scenarios

What-if on everything

Change any input — trades, market data, or collateral terms — and see the XVA impact on the fly. Run from the UI or via the REST API from your front-office system.

Trade What-If

- Novation impact

- Partial unwind

- New trade incremental

- Full portfolio unwind

Market Data

- Scalar bumps

- Curve shifts and bumps

- Volatility surface/cube shifts

- Absolute and relative

CSA Changes

- Threshold adjustment

- MTA change

- Discount curve switch

- Collateral currency

Custom Scenarios

- Combine any changes

- Regulatory stress sets

- Historical scenarios

- Save & replay

How It Runs

Distributed.

Cloud-native.

No vendor lock-in.

The Everix XVA engine runs on automatically deployed infrastructure — on-premises, your cloud provider, or our cloud. The same pipeline works on a single server for smaller books.

Consolidated View

All charges in one place

See XVA, Initial Margin, SA-CCR, and liquidity costs side-by-side. Marginal and forward versions of almost all metrics available. Export to CSV at any hierarchy level.

Related Solutions

SA-CCR

Standardised Approach for Counterparty Credit Risk — marginal, forward, pre-trade impact.

ExploreISDA SIMM™

ISDA-certified Initial Margin calculator with backtesting, what-if, and IM forward.

ExploreIFR / IFD

EU/UK capital requirements for investment firms — K-factors, own funds, and regulatory reporting.

ExploreGet Started

See XVA in your portfolio

We'll walk you through the platform with a real use case, listen to your setup, and tell you honestly if Everix is the right fit.